What cash offers (and doesn't)

When we talk about cash, we’re not referring to the coins and notes in your pocket or the money you spend on day-to-day expenses. We’re talking about choosing to save for the future in an account that pays you interest. This is usually with a bank, but it also covers money-market funds offered by investment companies, fixed-rate deposits and notice accounts.

Money market funds, fixed-rate deposits and notice accounts carry more risk than holding cash in a bank account. These risks may include potential market fluctuations or penalties for early withdrawal.

The benefits of cash

The big one for most people is that you’re very unlikely to lose money. When you put money in a cash account, you can be confident you’ll be able to take it out again – and there shouldn’t be less in there than you started with. (Though we do suggest you read our article on inflation to see how your money may not be quite as ‘safe’ as you think.)

Cash accounts are also great because you can normally take money out of your savings whenever you want. Some accounts do have restrictions on withdrawals, but they normally offer a higher interest rate in return, so you’re free to choose which is more important to you.

Finally, interest rates on most accounts are published by the banks. So, you know what you’re going to get – for a while, at least. This is very different to how it works with the vast majority of investments.

The drawbacks of cash

The benefits of cash are clear, but in our opinion, so is the big drawback. The interest rate you’ll receive is normally based on your country’s bank rate (also called the base rate in some countries). If rates are low, your savings won’t grow very much.

Even when rates are higher, they’re unlikely to match the returns you might receive from other investments. Of course, these investments do tend to involve more volatility (sudden rises or falls in value) and investment risk (the chance of losing money) – but their growth potential is also significantly higher.

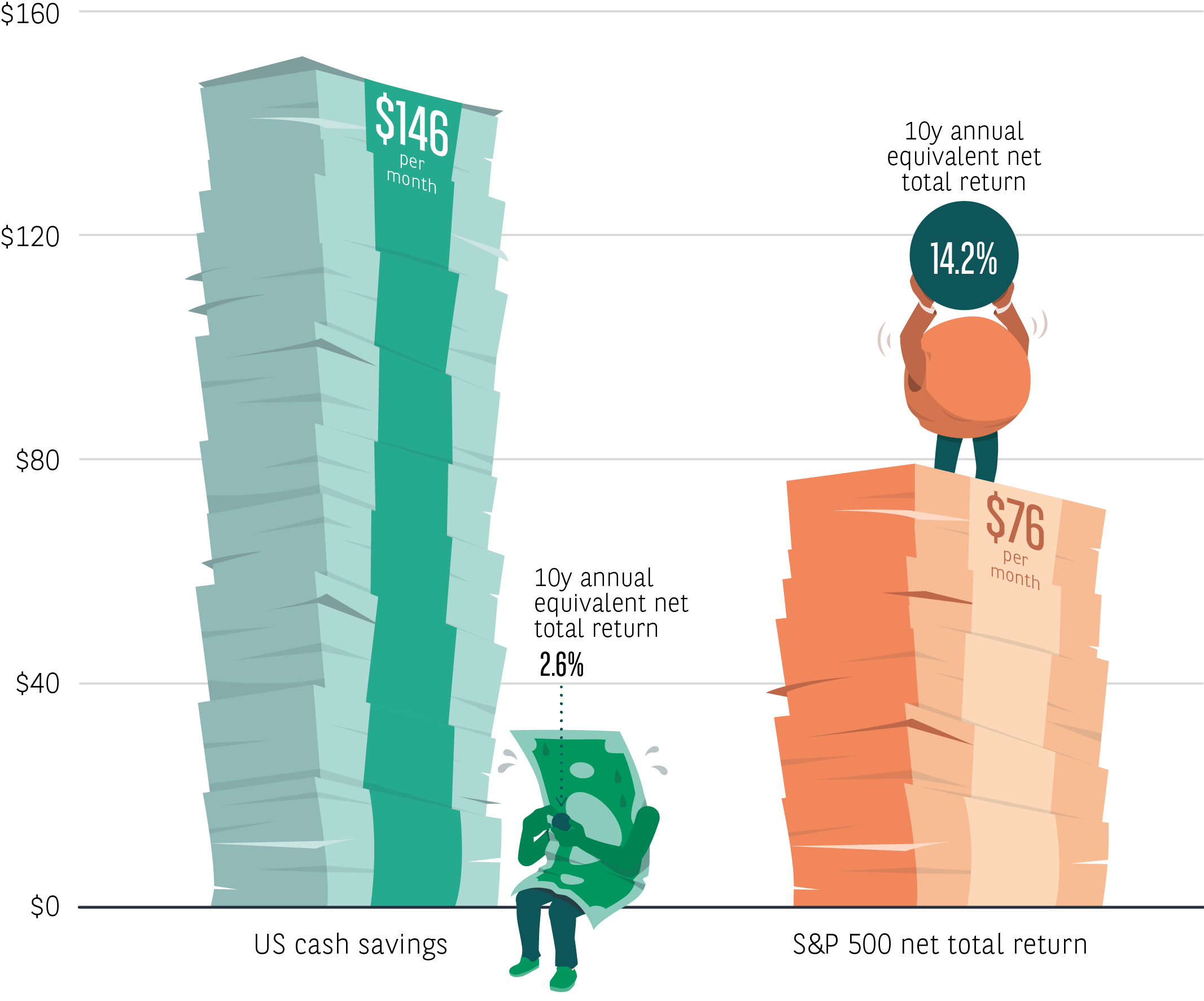

The impact of higher growth potential on your savings can be significant. We explore this is in detail in another article, but here’s a quick example to show you what we mean. Imagine you need to save $20,000 for something important that’s ten years away. How much would you need to put aside each month to get there?

How much does it take to reach your goal?

We’ve done the calculations based on the interest rate you would have gained through a US cash savings account and the equivalent of the total return you would have gained through an investment in US shares, based on 10 years. With shares, you’d have put aside $76 a month. With cash, it would have been $146 a month. That’s a big difference! Plus, if you’re putting less aside each month to reach your goal, you have more to spend on everything else.

Monthly contribution required to reach $20,000 over last 10 years

Source: Bloomberg, BNP Paribas Asset Management. Data from 31 December 2015 to 31 December 2025, US dollars. Past performance does not predict future returns.

As we’ve mentioned already, you do need to keep in mind that other types of investments can fall in value, particularly over the short term, which is why we’re talking about a long-term goal. Their performance is also more variable, so there aren’t any guarantees about how much you’ll make (though interest rates aren’t guaranteed over the long term either). Want to learn more about investing? Download our guide or keep reading the other articles in the Don't sit on your cash series.

Don’t sit on your cash

Download our guide for information on stepping off the sidelines and into the investment world

Download the guide

More articles from our Don't sit on your cash mini-series